9.15 Kelly Rejects Bad Trades Automatically: Why Overbetting Kills and Underbetting Doesn't

Kelly gives the growth-optimal bet size, outputs "no trade" when the edge is too thin, and punishes overbetting with ruin while underbetting only costs growth. Bet small, often, and never the negative-f* trades.

You found a real arbitrage. The article "Arbitrage Is Just Projection" handed you the trade, the guaranteed profit, and the target prices. None of that tells you how much to bet, and the sizing decision destroys more accounts than bad trade selection. Size too small and you leave growth on the table, survivable and boring. Size too large and you go broke holding a positive edge, which is the outcome nobody expects and plenty of people reach. Kelly gives the growth-optimal fraction, and read correctly it does two things most sizing rules do not: it tells you when a trade is not worth taking at all, and it makes the penalty for guessing wrong asymmetric in a way that should terrify you into betting less.

The formula, and where every input comes from

Bet a fraction of your bankroll each round on a bet that pays b per dollar risked when you win, with win probability p. Your wealth after a round is either multiplied up or cut down, and over many rounds what compounds is the log of those multipliers. Maximize the expected log-growth.

$$ G(f) = p \ln(1 + fb) + q \ln(1 - f), \qquad q = 1 - p $$

G is the long-run growth rate as a function of the fraction f you bet. The first term is the win branch weighted by its probability, the second the loss branch. Set the derivative to zero and the maximizer falls out clean.

$$ f^* = \frac{pb - q}{b} = p - \frac{q}{b} $$

Three inputs, nothing hidden. The p is your estimated win probability, q is one minus that, and b is the profit per dollar risked on a win. Everything in the sizing decision reduces to those three numbers, which means every sizing error reduces to an error in one of them.

Three worked cases show the range of what the formula says.

Even-money bet, b equals 1, so the formula collapses to 2p minus 1. Estimate a 55 percent win rate and f-star is 0.10. Bet 10 percent of capital per round. Standard textbook result.

Prediction-market arbitrage, guaranteed profit of 8 cents per dollar deployed, so b is 0.08, and execution reliability pulls the effective win probability to 0.90. Now f-star is 0.90 times 0.08 minus 0.10, all over 0.08, which is negative 0.35.

$$ f^* = \frac{0.90 \times 0.08 - 0.10}{0.08} = \frac{0.072 - 0.10}{0.08} = -0.35 $$

Negative. A negative Kelly fraction is not a short signal; it is a refusal. The execution risk is too high for the thin margin, and the formula says do not put money on this. Most sizing tutorials never mention that Kelly outputs "no trade," and it is the most useful thing it does. The article "The Six Ways to Lose Money on Polymarket" catalogs traders who took this exact trade anyway because 8 cents looked free.

Same 8-cent profit, but execution is nearly certain, p equals 0.99. Now f-star is 0.865: bet 86.5 percent of capital. Correct, and insane. Nobody sane bets 86 percent of their bankroll on one trade, which is the entire reason fractional Kelly exists and full Kelly does not get deployed raw.

What Kelly promises, and the variance it hides

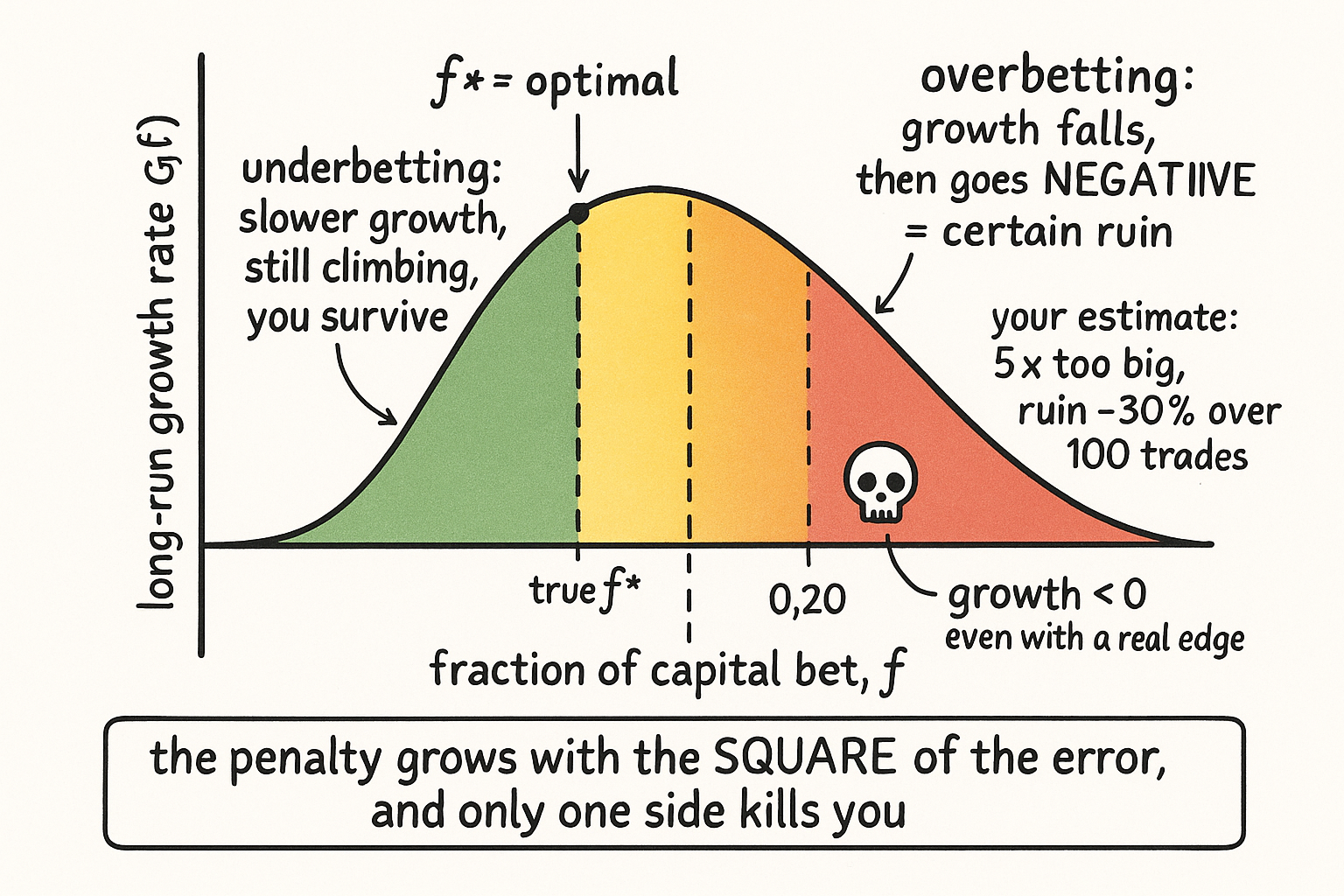

The Breiman results are the reason Kelly is the reference point. Among all fixed-fraction strategies, f-star maximizes the long-run growth rate almost surely, reaches any wealth target in the least expected time, and never risks total ruin, because f-star stays below 1 whenever you have a positive edge. Optimal growth, minimum time, no ruin. It sounds like a free lunch.

The bill is variance. A 55 percent even-money bettor sizing at the full f-star of 0.10 sees drawdowns past 50 percent at the 10th percentile over a thousand rounds. Half your capital gone, one time in ten, running the mathematically optimal strategy with a genuine edge. And that assumes you know p and b exactly, which you never do. Full Kelly is the growth-optimal size for a world where your inputs are perfect. That world does not exist.

The penalty is quadratic, and it only bites in one direction

Bet the wrong fraction, off from optimal by an amount delta, and the growth rate drops.

$$ G(f^* + \Delta) \approx G(f^*) - \frac{\Delta^2}{2\sigma^2} $$

The loss in growth is proportional to the square of the sizing error. Small misses barely register: a delta of 0.02 costs almost nothing. Large misses compound: a delta of 0.15 can drive the growth rate below zero, and below zero means you go broke over time even with a real edge. The square is the whole story, because it means being twice as wrong is four times as costly.

The asymmetry is what turns a math result into a survival rule. Overbetting and underbetting are not mirror images.

Underbet, f below f-star, and growth slows but stays positive. You compound more slowly, you never blow up. Overbet, f above f-star, and growth falls, then past a threshold turns negative, and negative growth is certain ruin. One direction is slow. The other is fatal.

The numbers make it concrete. True edge supports f-star of 0.04, but you estimate 0.20, a 5-times overbet. That is not an exotic error; it is what happens when you take a noisy edge estimate at face value. Over 100 trades at that size, the probability of ruin exceeds 30 percent. You had a real, positive edge and a one-in-three chance of being wiped out, entirely from sizing.

$$ \text{true } f^* = 0.04, \quad \hat{f}^* = 0.20 \;\Rightarrow\; 5\times \text{ overbet} \;\Rightarrow\; P(\text{ruin over 100 trades}) > 30\% $$

Fractional Kelly, and the arbitrage-specific version

Because you never know your edge exactly, you bet a fraction of the fraction. The tradeoff table is the practical core of the chapter.

$$ \begin{array}{lccl} \textbf{Fraction} & \textbf{Growth vs full} & \textbf{Variance} & \textbf{When to use}\\ 1.0 \times f^* & 100\% & \text{high} & \text{edge is precisely known (it never is)}\\ 0.5 \times f^* & 75\% & \sim 50\% \text{ lower} & \text{moderate estimation error}\\ 0.25 \times f^* & \sim 44\% & \sim 75\% \text{ lower} & \text{edge estimate is uncertain} \end{array} $$

Read the middle row. Half-Kelly keeps 75 percent of the growth while cutting variance roughly in half. You give up a quarter of your growth to halve the chance of a brutal drawdown, and given the asymmetry above, that is a trade worth making every time. The rule of thumb: structural arbitrage, where the edge is derived from the geometry rather than forecast, can carry 0.5 to 0.75 times Kelly because the edge estimate is tighter; informational edge, where you are guessing at a probability, gets 0.25 to 0.5 times because the estimate is soft. The article "Bayesian Edge in Log-Odds" is where that softness gets measured, and the shrinkage it prescribes is the same instinct as fractional Kelly applied one layer up.

Structural arbitrage needs one more adjustment, because the guaranteed profit is only guaranteed if you actually fill both legs.

$$ f_{\text{arb}} = f^* \times P(\text{full execution}) \times (1 - s) $$

Take the Kelly fraction, scale it by the probability that all legs fill, then scale again by one minus the slippage as a fraction of the edge. A trade with a clean geometric edge but a 60 percent full-fill probability and slippage eating a fifth of the margin gets sized far below its naive Kelly number. And cap the position at half the order-book depth regardless, because a position larger than that moves the market against you as you build it, which is its own tax measured in the article "Execution Is Part of Expected Value."

The real accounts confirm the shape. Reconstructing the top Polymarket account from its profit and win-rate statistics puts per-trade notionals in the low thousands of dollars against a capital base in the hundreds of thousands, well under 1 percent of capital per trade. That is not timidity. That is fractional Kelly plus aggressive diversification across many small, high-certainty structural bets, which is how a 90-plus percent win rate compounds into seven figures without a ruinous drawdown. The edge was never in betting big. It was in betting small, often, and never taking the negative-f-star trades.

KEY POINTS

- Kelly sizes for growth-optimal compounding: f-star equals p minus q over b, using your win probability p and the profit per dollar b. Every sizing error is an error in one of those inputs.

- A negative f-star is a refusal, not a short. The arb example with 8-cent profit and 90 percent execution gives f-star of negative 0.35, which means do not trade. Kelly outputting "no trade" is its most useful and most ignored feature.

- Breiman: f-star maximizes long-run growth, reaches targets fastest, and never fully ruins you. The cost is variance, with 50-percent-plus drawdowns at the 10th percentile even at full Kelly with a real edge, and it assumes inputs you never have exactly.

- The growth penalty is quadratic in the sizing error, so twice as wrong is four times as costly. And it is asymmetric: underbetting slows growth but survives, overbetting past a threshold turns growth negative, which is certain ruin.

- A 5-times overbet (true f-star 0.04, estimated 0.20) carries over 30 percent ruin probability across 100 trades, with a genuine positive edge. This asymmetry is the entire case for fractional Kelly.

- Use half-Kelly to keep 75 percent of growth at half the variance. Structural edge takes 0.5 to 0.75 times, informational edge 0.25 to 0.5 times. For arbitrage, scale further by fill probability and slippage, and cap at half the book depth. The top real account sized well under 1 percent per trade and diversified hard.