9.33 The $40M, Verified: Reading the Probabilistic-Forest Arbitrage Paper

A year of Polymarket data, $40M in arbitrage. But almost all of it is plain single-market rebalancing harvested by a few bots during volatility, not the exotic cross-market kind.

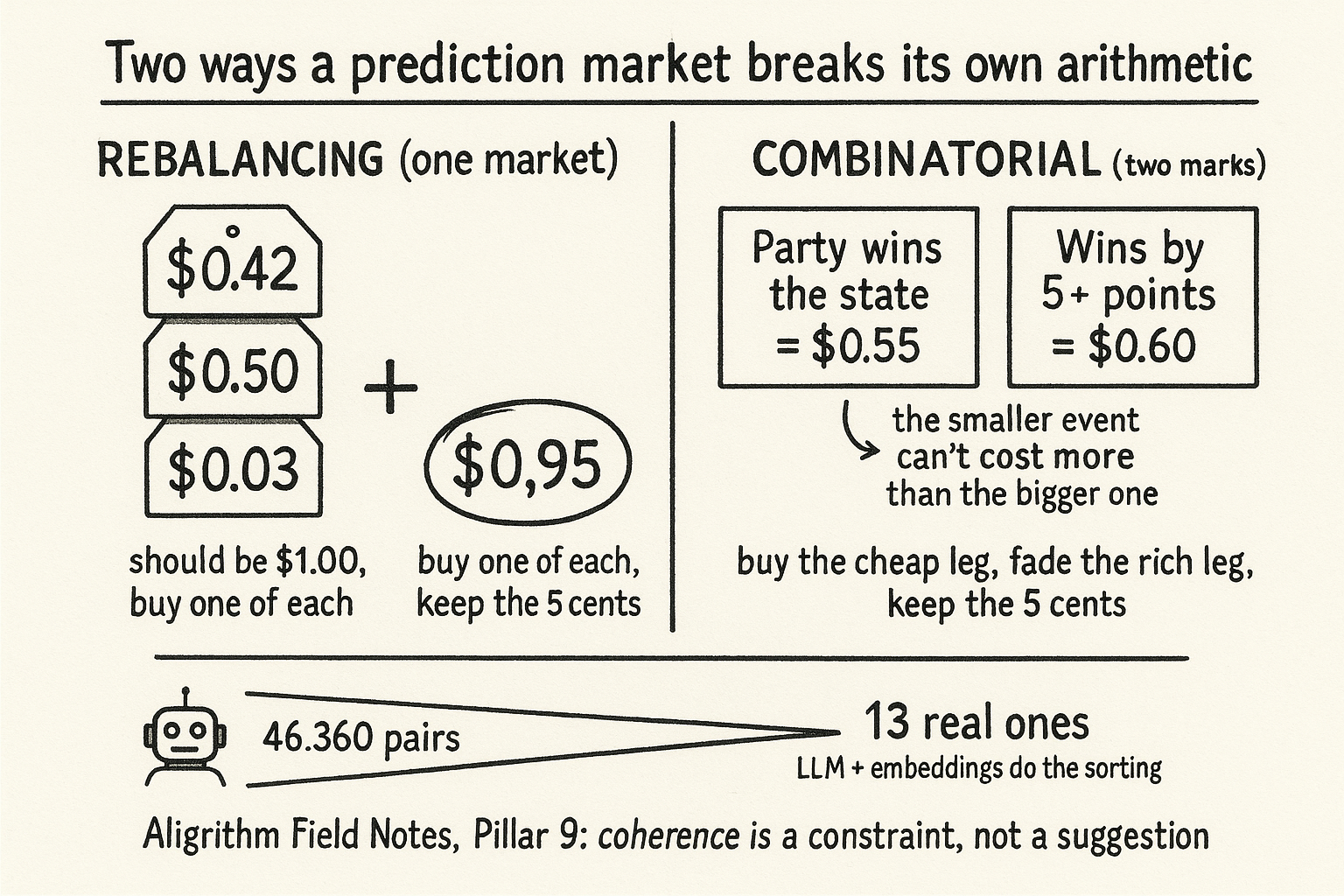

Take a market with three mutually exclusive outcomes: a Republican wins New York, a Democrat wins, or a third party wins. Exactly one of those pays $1 at resolution, the other two pay nothing. So the three YES prices have to add up to $1. If a trader can buy one share of each for a combined $0.95, they lock in a nickel of guaranteed profit before knowing who wins. That gap is not a forecast and not a bet. It is a bookkeeping error someone left on the table.

Oriol Saguillo and coauthors went looking for those errors across a year of Polymarket data, April 2024 to April 2025, and put a number on them: about $40 million extracted. The old article "The Marginal Polytope: One Shape That Contains Every Fair Price" argued the theory of this, that every coherent set of prices has to live inside one convex shape, and that stepping outside it is a free lunch. This paper is the empirical audit. It counts how often prices stepped outside, how much money was sitting there, and whether anyone actually picked it up. My job here is to read the pipeline they built, check what the $40M is made of, and separate the parts that generalize from the parts that were a one-time election windfall.

The one rule the whole thing rests on

A Polymarket market is a question with a set of conditions, and the conditions are built to be exhaustive and mutually exclusive: one and only one resolves True. The price of a YES token is read as the market-implied probability of that outcome. Stack the definition together and you get a hard constraint on the prices.

$$ \sum_{i} \mathrm{val}(Y_i, t) = 1 $$

This says the YES prices of all the conditions in a market, summed at any single moment t, must equal $1. It is the same statement as "probabilities of a complete, mutually exclusive set of outcomes add to one," dressed in trading-token clothes. Work a number through it. A New York election market lists three conditions priced at Republican $0.42, Democrat $0.50, third party $0.03. Those sum to $0.95, not $1. The market is quoting a 95% chance that somebody wins the election it was built to cover, which is nonsense, because somebody wins with certainty. The missing 5 cents is the error, and the constraint is what tells you it is an error rather than an opinion.

Two ways the sum breaks

The paper splits arbitrage into two clean types by where the incoherence lives. The first is Market Rebalancing Arbitrage, inside a single market. When the YES prices sum below $1, you buy one share of every condition and wait.

$$ \text{Long: } \sum_{i} \mathrm{val}(Y_i, t) < 1 \qquad \text{profit} = 1 - \sum_{i} \mathrm{val}(Y_i, t) $$

Buying all three New York conditions costs $0.95. One of them resolves to $1, the other two to $0. You paid $0.95 and collect $1, so the guaranteed profit is $0.05 per set, independent of who actually wins. The mirror case runs the other way. When the YES prices sum above $1, the NO tokens are the underpriced side.

$$ \text{Short: } \sum_{i} \mathrm{val}(Y_i, t) > 1 \qquad \text{profit} = \sum_{i} \mathrm{val}(Y_i, t) - 1 $$

Say the same three conditions instead sum to $1.08. Buy one NO for each condition. Across three mutually exclusive outcomes, exactly one YES wins, so exactly two NO tokens pay $1 each, giving $2 total. The NO tokens cost the complement of the YES prices, which is 3 minus $1.08, or $1.92. You collect $2 against $1.92 paid, banking $0.08, again the exact size of the overshoot. Both directions pay you the distance between the price sum and $1, and the paper found the overwhelming majority of single-condition opportunities were long, meaning prices summed below $1.

The second type is Combinatorial Arbitrage, and it spans two markets whose outcomes are logically linked. A market on "which party wins the state" and a market on "the winning margin" are not independent: winning by 5 or more points is a subset of winning at all, so its price can never sit above the price of winning.

$$ \text{Arbitrage if } \quad \sum_{c \in S} \mathrm{val}(T_c, t) \neq \sum_{c' \in S'} \mathrm{val}(T_{c'}, t) $$

The dependent subset S in one market and S' in the other must carry the same total probability, so any gap between the two sums is money. Concrete version: "Republican wins the state" trades at $0.55, while "Republican wins by 5 or more" trades at $0.60. The narrower event is priced richer than the broader event that contains it, which is impossible if the market is coherent. Buy the cheap leg, take the opposing position on the rich leg, and the $0.05 gap is locked regardless of the final margin. The profit is the difference in the two dependent sums, same shape as rebalancing, just read across two order books instead of one.

The scaling wall, and the triage that gets around it

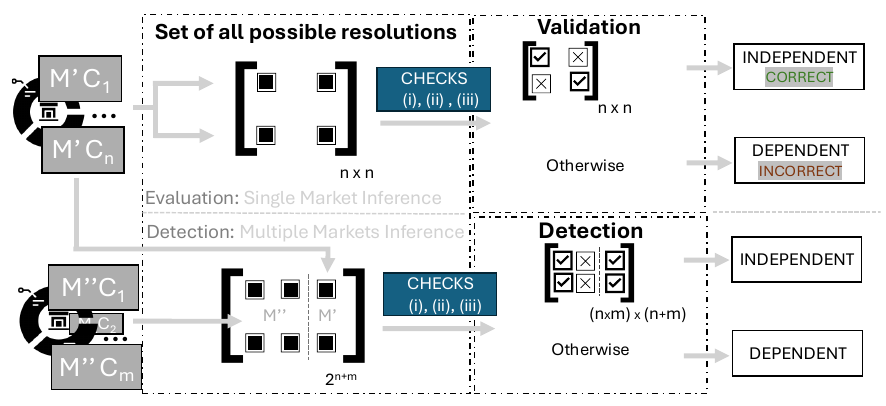

Finding the first type is cheap, because you only look inside one market. Finding the second type is where the paper earns its keep, because you have to check pairs of markets for hidden logical dependence, and the honest way to do that blows up fast.

$$ \text{naive comparisons per market pair} = O\!\left(2^{\,n+m}\right) $$

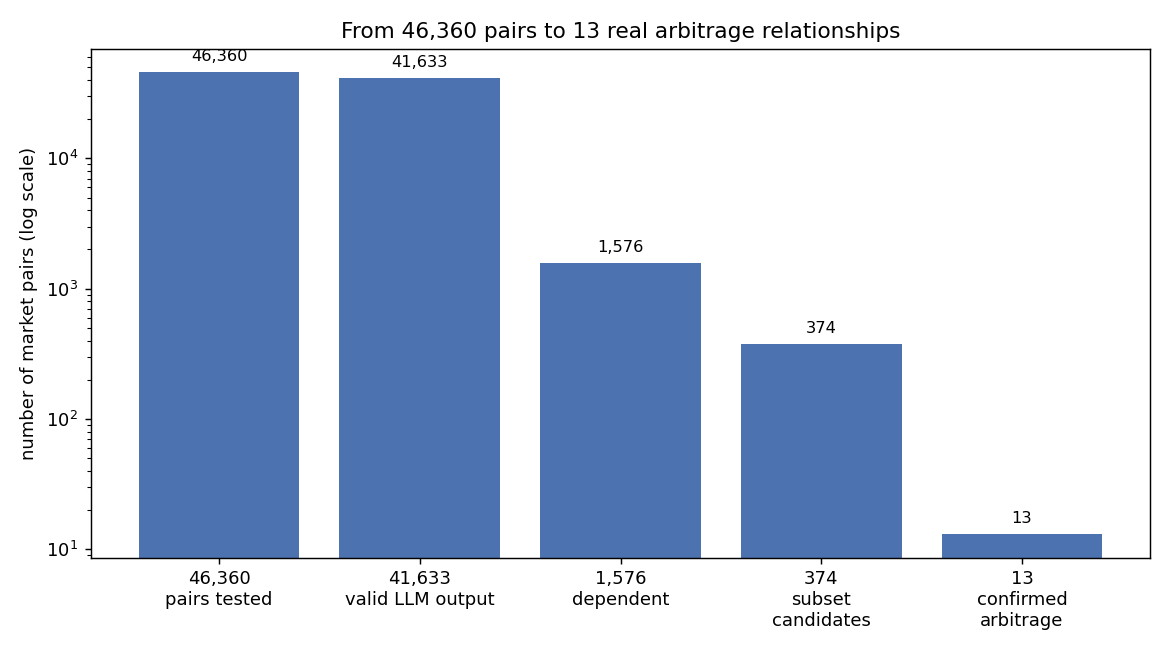

For two markets with n and m conditions, the joint space of True/False assignments has 2 to the power of n plus m entries, and something has to reason over all of them to decide whether the two markets constrain each other. Take a pair where each market has 5 conditions: 2 to the power of 10 is 1,024 combinations for that one pair. Now recall the election group alone held 46,360 candidate pairs. Enumerating 1,024 combinations across 46,360 pairs is roughly 47 million reasoning steps, and that is before you widen n and m past 5. No human checks 46,360 pairs, which is the whole point of the old article "46,360 Pairs No Human Can Check."

The authors cut the space with three filters stacked in order. First, timeliness: only compare markets that share the same end date, since Polymarket markets about the same event are created to resolve on the same day. Second, topic: run each market's question through the Linq-Embed-Mistral text embedder, the best open-source embedder on the MTEB leaderboard at the time, take cosine similarity against seven topic labels (Politics, Economy, Technology, Crypto, Twitter, Culture, Sports), and only compare markets inside the same topic. A hand-check of 100 labels put topic accuracy at 92%. Third, and this is the load-bearing trick, hand the reduced condition sets to a large language model, DeepSeek-R1-Distill-Qwen-32B, and ask it to return the set of valid joint outcomes as strict JSON, using chain-of-thought reasoning to work out which combinations are logically impossible.

The LLM has a real limit the paper does not hide: it chokes past four or five conditions. On the single-market sanity check, where every condition is dependent by construction, 128 markets went in and only 101 (81.45%) came back fully correct, with 4 returning invalid JSON and the rest failing the outcome-vector checks. When a market has too many conditions, the model falls into a reasoning loop and tries to spit out the full 2-to-the-power exhaustive table, the exact explosion the pipeline was built to avoid. The fix is blunt: reduce any market to its top four conditions by traded volume plus a fifth catch-all "everything else" condition. Over 90% of a market's liquidity sits in the top four conditions, so the reduction loses little, and the fifth condition preserves the logical dependencies by standing in as a logical OR of the tail.

The funnel is brutal. Of 46,360 election pairs, 353 returned no JSON and 4,374 returned malformed output, leaving valid results on the rest. The LLM tagged 40,057 pairs as independent and 1,576 as dependent. A subset checker cut the 1,576 down to 374 that could structurally hold arbitrage, and a manual pass over those 374 confirmed 13 pairs that satisfy the strict combinatorial definition, 11 NegRisk-to-NegRisk and 2 NegRisk-to-Single. Outside the election, 2,267 pairs produced exactly one dependent pair, and that one did not even meet the strict definition. Thirteen real relationships out of tens of thousands of candidates. Keep that ratio in mind when you read the headline number.

Did anyone actually take it

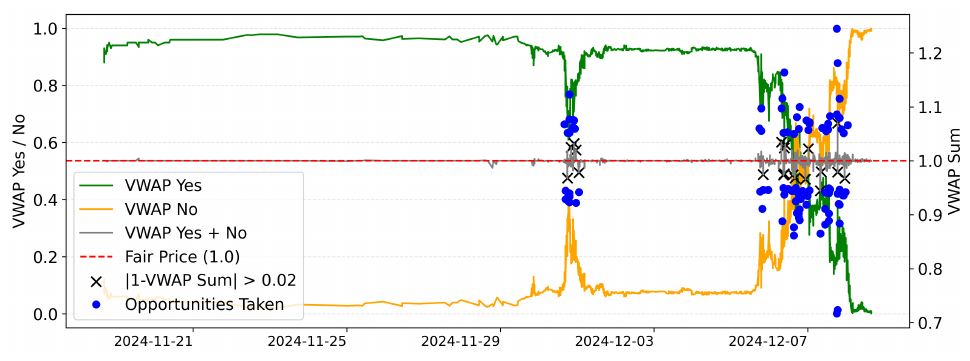

Opportunities existing is not money made. The paper reconstructs 86 million on-chain bids, computes a volume-weighted average price per token per block, and flags an opportunity when the absolute gap between the price sum and $1 exceeds two cents, restricting to moments when no outcome is already priced above $0.95 (so the event is still live and liquid). Then it checks which addresses actually held the winning basket of positions inside a roughly one-hour window.

The example condition shows the mechanism plainly: the YES and NO prices sit calm and coherent for weeks, then the sum lurches away from $1 during a burst of volatility, and blue markers show traders stepping in during exactly those windows. Arbitrage is a volatility phenomenon here. When nothing is happening, the book stays coherent and there is no gap to harvest.

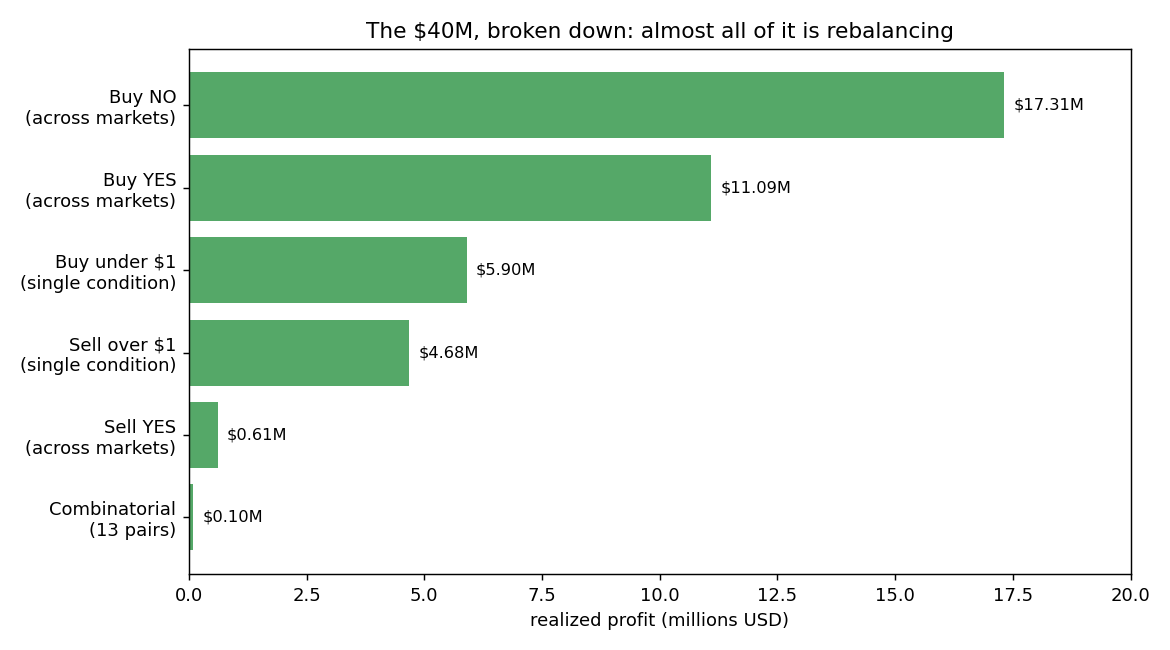

Adding the strategies up gives $39,587,585, call it $40 million, under the paper's assumption of at least $1 profit per counted trade. The composition matters more than the total. Buying NO positions across multi-condition markets brought in $17.3M and buying YES another $11.1M; single-condition rebalancing added $5.9M on the buy side and $4.7M on the sell side. Combinatorial arbitrage, the exotic cross-market type that needed the whole LLM pipeline to find, extracted about $95,000 across five of the 13 pairs. The clever part of the paper produced a rounding error of the profit. Almost all $40M is plain single-market rebalancing that needs no embeddings and no language model, only a script that adds up prices and notices they miss $1.

The extraction is also concentrated. The top account cleared $2.0M across 4,049 trades, the top ten accounts show bot-like trade counts in the thousands, and only about 1% of the estimated election-window opportunities were ever taken. One trader, @Tutaaa91, bought both sides of a condition for under $0.02 each and booked $58,983 on a single trade when prices detached from any real probability. This is not a crowded, efficient market grinding out basis points. It is a thin field of a few automated players cleaning up obvious mistakes, with most of the theoretical money never touched.

What survives the skepticism

Three caveats keep this from being a repeatable strategy pitch. First, the window is a single 2024-25 US election cycle, the most liquid event in Polymarket's history at over $3.7 billion in volume, and the profit concentrates there. The old article "$40M, One Election Cycle: Where Did the Arbitrage Come From?" makes the point that this is a snapshot, not a run rate. Strip the election and the numbers shrink hard.

Second, every leg is non-atomic. On an order-book venue you place one order, then another, and the second can fail after the first fills, so the "guaranteed" profit carries real execution risk that the clean inequalities above ignore. This is not a DeFi flash-loan swap that reverts if any leg misses. You can get stuck holding half a position.

Third, the $40M is a floor built from volume-weighted average prices, which smooth away the sharpest intrabar dislocations, so the paper underestimates the margin an alert bot actually captured, while also counting gross profit with no accounting for the capital tied up or the tail of trades that lost. The honest read: incoherence on Polymarket is real, common in single markets, and mostly harvested by a handful of bots during volatility spikes, while the cross-market combinatorial arbitrage that makes the paper novel is rare, hard to find, and barely worth money so far. The pipeline is the contribution. The $40M is mostly the easy kind.

Where this connects

This paper is the empirical body attached to the theory head of the old article "The Marginal Polytope: One Shape That Contains Every Fair Price." The polytope says coherent prices live inside one convex hull; Saguillo and coauthors measured how far and how often Polymarket prices sat outside it, and who profited from dragging them back in. The combinatorial-explosion filter, temporal proximity plus topical embeddings plus an LLM reading logical dependencies, is the practical answer to the structural moat described in the old article "46,360 Pairs No Human Can Check," and the composition of the profit is the receipt for the framing in the old article "$40M, One Election Cycle: Where Did the Arbitrage Come From?" Read together, the lesson is narrow and useful: the coherence constraint is enforceable and enforced, but the enforcement is thin, automated, and concentrated in the loudest event of the year, not a standing river of alpha you can wade into.

KEY POINTS

- A prediction market's mutually exclusive YES prices must sum to $1. When they sum to less, buy one share of each condition and keep the shortfall; when they sum to more, buy the NO side and keep the overshoot. The profit is the exact distance from $1.

- Market Rebalancing Arbitrage lives inside one market and is trivial to spot. Combinatorial Arbitrage spans two logically linked markets, where a narrower outcome is priced above the broader outcome that contains it.

- Checking every market pair for hidden dependence scales like 2 to the power of n plus m per pair, which is hopeless across 46,360 election pairs. The paper cuts it with same-end-date filtering, Linq-Embed-Mistral topic embeddings, and a DeepSeek LLM that returns valid joint outcomes as JSON.

- The LLM breaks past four or five conditions and falls into reasoning loops, so markets are reduced to their top four conditions by volume plus a catch-all fifth, which holds over 90% of liquidity.

- The funnel goes 46,360 candidate pairs to 1,576 dependent to 374 structural candidates to 13 confirmed combinatorial relationships. Real cross-market arbitrage is rare.

- The realized total is about $40M over April 2024 to April 2025, but roughly $39.9M of it is plain single-market rebalancing. Combinatorial arbitrage, the novel part, extracted only about $95,000 across five pairs.

- Extraction is concentrated in a few bot-like accounts, only about 1% of opportunities were ever taken, every leg is non-atomic and carries execution risk, and the whole figure is a single election-cycle snapshot, not a run rate.

References

- Prediction Markets (Wolfers and Zitzewitz, 2004)

- Flash Boys 2.0: Frontrunning, Transaction Reordering, and Consensus Instability in Decentralized Exchanges (Daian et al., 2020)

- Quantifying Blockchain Extractable Value: How Dark Is the Forest? (Qin, Zhou, and Gervais, 2022)

- Non-Atomic Arbitrage in Decentralized Finance (Heimbach, Pahari, and Schertenleib, 2024)

- Automated Market Making and Arbitrage Profits in the Presence of Fees (Milionis, Moallemi, and Roughgarden, 2024)

- Chain-of-Thought Prompting Elicits Reasoning in Large Language Models (Wei et al., 2022)

- DeepSeek-R1: Incentivizing Reasoning Capability in LLMs via Reinforcement Learning (Guo et al., 2025)

- Unravelling the Probabilistic Forest: Arbitrage in Prediction Markets (Saguillo, Ghafouri, Kiffer, and Suarez-Tangil, 2025)