9.30 The Term Structure of Strategy: Momentum Far Out, Reversion Near Resolution

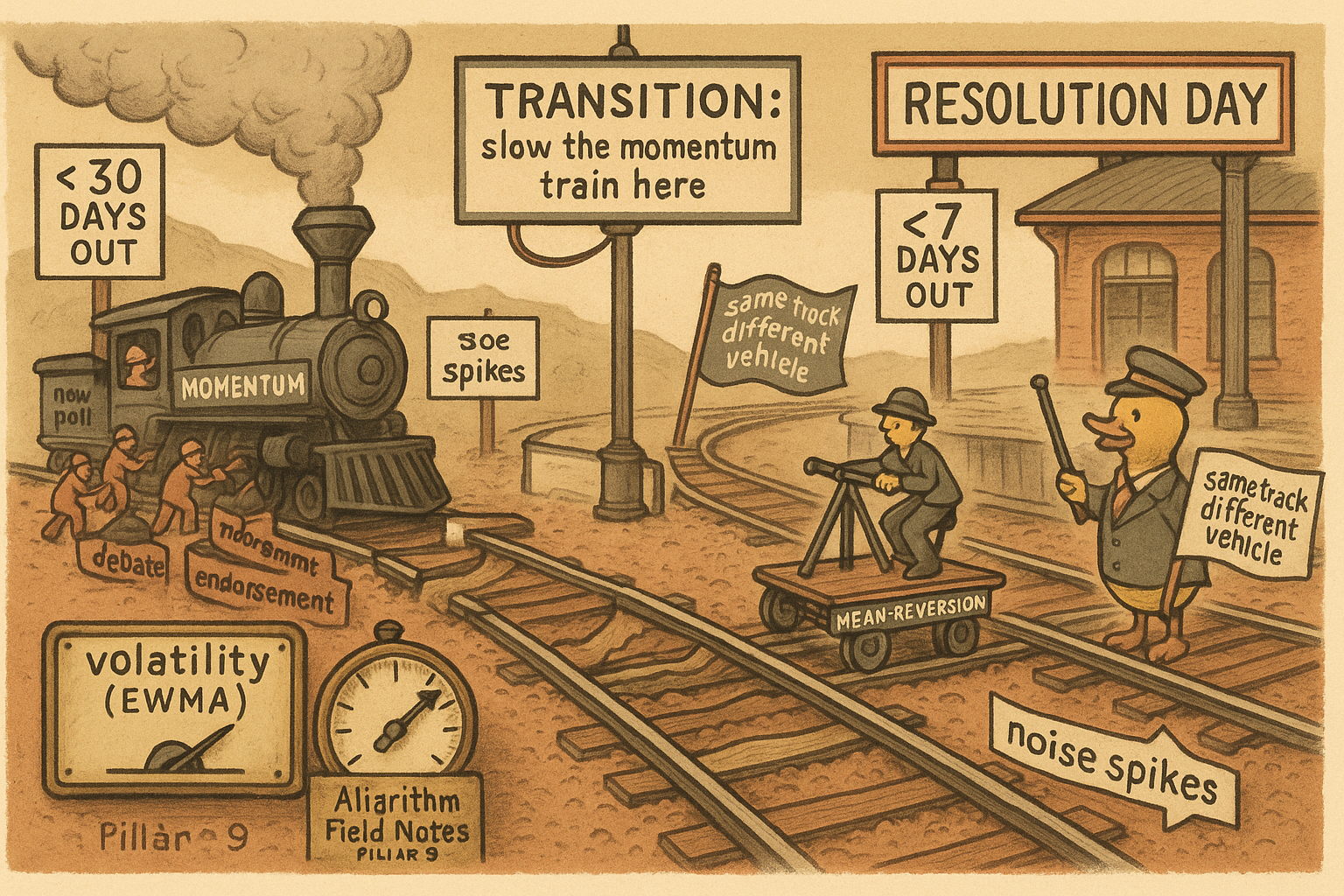

A prediction market resolves to 0 or 1 on a fixed date, and that wall flips the strategy. More than 30 days out prices trend, so momentum pays. Inside 7 days prices overreact to noise, so reversion pays.

A momentum rule that printed money on an election market sixty days out will hand it all back in the final week. Same market, same rule, opposite result, and nothing about your code changed. What changed is the distance to resolution, and that distance flips which strategy pays. A prediction market is not one environment. It is a sequence of them, ordered by time-to-resolution, and the strategy that fits at the far end is the strategy that bleeds at the near end.

This is the piece of the regime story that is specific to prediction markets and has no clean analog in FX or equities. The full regime treatment, including crowding and the winner-take-most concentration of arbitrage profit, lives in the article "The Term Structure of Prediction-Market Strategy and Crowding: Why the Fastest 3 Bots Take 80%." Here the scope is one axis: calendar time before the contract settles.

Why prediction markets have a term structure at all

A stock has no forced destination. A prediction-market contract does. It resolves to exactly one dollar or exactly zero on a known date, and the price is a probability crawling toward one of those two walls. That terminal boundary is what gives the market a term structure of behavior, because the character of price movement depends on how much genuine information is left to arrive before the wall.