9.37 Bold vs Timid: The Math of Betting When You Must

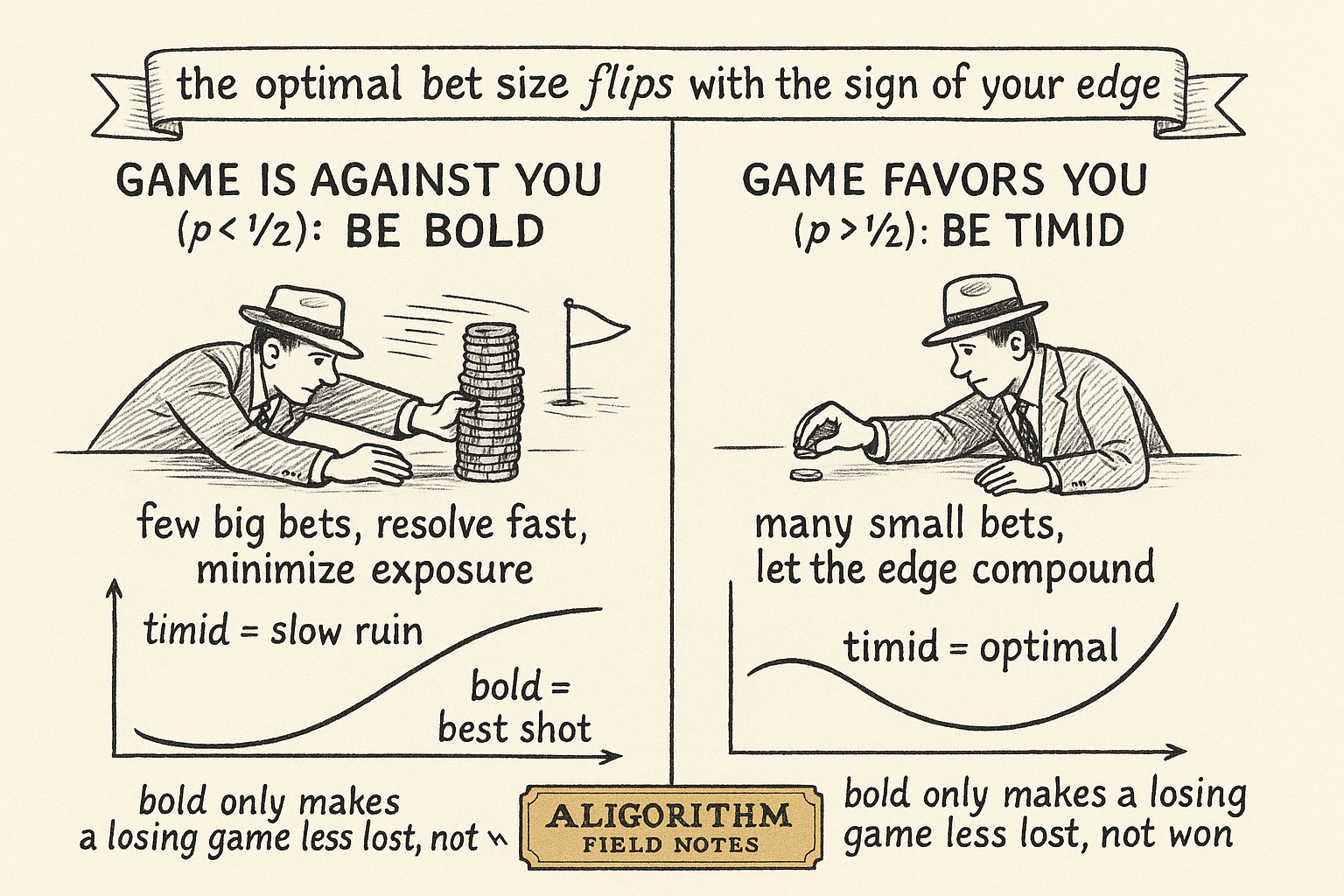

When the game is against you, betting small is slow suicide. Bold play, swinging your whole stack at the target, maximizes your chance of hitting it. Optimal bet size flips with the sign of your edge.

Here is a result that offends every instinct a careful trader has. You are in a game that is rigged against you, a small negative edge on every bet, and you have to turn a starting stake into a target before you go broke. The disciplined move feels obvious: bet small, spread the risk, give the law of large numbers time to work. That instinct is exactly backwards. Kyle Siegrist's expository treatment of the red-and-black problem proves that when the game is unfair, the strategy that maximizes your chance of hitting the target is bold play: bet your whole fortune, or just enough to reach the goal, on every single game. Grinding small bets, timid play, is provably the worst thing you can do. It hands you a near-certain slow death.

This is not a trick or an edge case. It is a theorem, and it flips again when the game turns in your favor. If you have a real edge, bet tiny. If you are behind the house, bet everything. The whole content of "how to gamble if you must" is that the optimal bet size depends on the sign of your edge in a way that has nothing to do with growth rate and everything to do with the geometry of absorbing barriers. That distinction matters because a trader in a funded-account challenge, or anyone trying to hit a fixed target before a drawdown floor, is playing exactly this game, and the Kelly reflex from the old article "Kelly Rejects Bad Trades Automatically: Why Overbetting Kills and Underbetting Doesn't" is answering a different question than the one on the table.

Every bet you make bleeds you

Start with the one fact that governs everything. Let your fortune after game n be X-n, and let Y-n be the amount you wager on game n in a game you win with probability p. The expected change in your fortune per bet is fixed.

$$ \mathbb{E}(X_n) = \mathbb{E}(X_{n-1}) + (2p - 1)\,\mathbb{E}(Y_n) $$

Read it plainly. Whatever you bet, your expected fortune moves by two-p-minus-one times the stake. When p is below one half the multiplier is negative, so every dollar you put at risk loses money on average; when p is above one half it gains; when p equals one half it is a martingale that drifts nowhere. Work a number: at p equal to 0.45 you wager 10 dollars, and your expected change is 2 times 0.45 minus 1, which is minus 0.10, times 10, so minus one dollar. Every ten dollars through the game costs you one dollar in expectation.

Now chain the logic. Your total expected loss is that edge times the total volume you wager over the whole session. If you want to minimize expected bleed, you minimize the number of dollars that pass through the machine, which means you want to reach the target or bust in as few bets as possible. Timid play does the opposite: it forces enormous volume through a losing edge. This is the seed of why bold wins. You are not trying to grow money, you are trying to touch a target before the edge grinds you to zero, and exposure is the enemy.

Timid play is gambler's ruin, and gambler's ruin is a trap

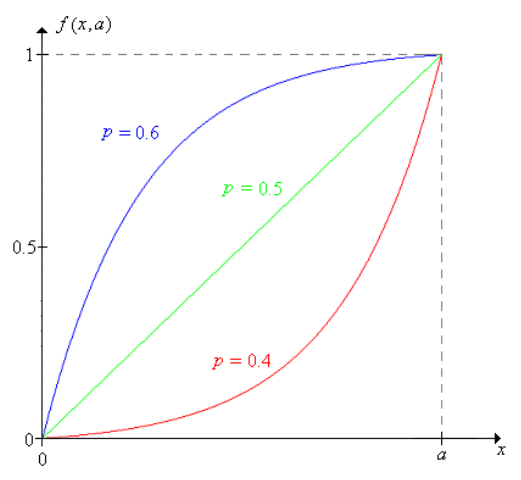

Timid play, betting one dollar a game until you hit zero or the target a, is a random walk with two absorbing barriers. The probability of reaching a from a starting fortune x has the classic gambler's-ruin form.

$$ f(x, a) = \frac{(q/p)^{x} - 1}{(q/p)^{a} - 1} \quad (p \ne \tfrac{1}{2}), \qquad f(x, a) = \frac{x}{a} \quad (p = \tfrac{1}{2}) $$

The letter q is one minus p, so q over p is the odds against you, a number bigger than one whenever the game is unfair. Because that ratio is raised to the power of your fortune, the success function is convex and hugs the floor: you need to climb almost all the way to the target before your odds of getting there become respectable. Work it at p equal to 0.45 with a target of 20 dollars, starting at 10, exactly half way. The ratio q over p is 1.222, so f is 1.222 to the tenth minus one, over 1.222 to the twentieth minus one, which is 6.44 over 54.4, about 0.118. You start at the halfway mark and still reach the goal only twelve percent of the time.

The figure is the paper's own picture of this. For p above one half the curve bulges upward and you are likely to win from almost anywhere; for p below one half it sags into the floor and you are doomed across most of the range; at exactly one half it is the straight diagonal, where your chance of success is just your fortune divided by the target. The old article "Kelly in Prediction Markets vs a Prop Challenge: Same Formula, Opposite Geometry" built the bridge from this gambler's-ruin barrier to a trading account with a hard floor. The lesson there and here is the same: a fixed barrier plus a negative drift is a machine for slow, near-certain ruin, and betting small only lets the machine run longer.

Bold play, the doubling map, and an exotic staircase

Bold play scales, so set the target to one dollar and let your fortune be a fraction x between zero and one. You bet the smaller of x and one minus x, driving straight for the goal. Condition on the first game and the success function F satisfies a functional equation instead of a linear difference equation.

$$ F(x) = \begin{cases} p\,F(2x), & 0 \le x \le \tfrac{1}{2} \\[4pt] p + q\,F(2x - 1), & \tfrac{1}{2} \le x \le 1 \end{cases} $$

The recursion says: from below the midpoint you must win the next game (probability p) and then you are playing bold from twice your fortune; from above the midpoint you either win outright with probability p or, failing that, restart from 2x minus 1. The doubling map, the operation that sends x to the fractional part of 2x, is doing the work, which is why bold play is secretly a dynamical system on the binary digits of your fortune. Work two values with p equal to 0.45: at x equal to one half, F is just p, so 0.45. At x equal to one quarter, F is p times F of one half, which is p squared, 0.2025. Compare that quarter-fortune bold number, 0.20, against the timid result, which from a quarter of a twenty-dollar target is a dismal few percent.

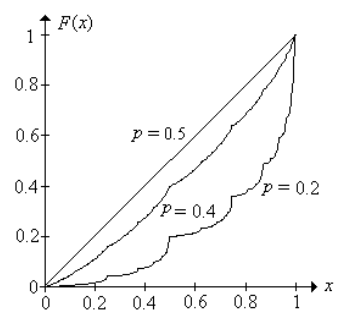

The strangest part is what the success function looks like across all starting fortunes. Write W as the number whose binary digits are the complements of the game outcomes.

$$ W = \sum_{j=1}^{\infty} \frac{1 - I_j}{2^{j}}, \qquad F(x) = \mathbb{P}(W \le x) $$

Each I-j is one if you win game j and zero if you lose, so W packs the entire sequence of outcomes into the bits of a single number between zero and one, and the bold success function is exactly the distribution function of W. When the game is fair, W is uniform and F is the plain diagonal. When p is not one half, W has a singular continuous distribution: F is continuous and strictly increasing, yet its derivative is zero almost everywhere. It is a devil's-staircase, all of its increase concentrated on a set of measure zero, the same kind of pathological object as the Cantor function, arising here from an honest casino question.

The paper's plot shows F for a few values of p, and you can see the staircase texture and the way the unfair curves bow below the diagonal. The point for a bettor is not the fractal beauty; it is that even this optimal bold curve sits below break-even when the game is against you. Bold is the best you can do, and the best you can do is still a losing proposition.

The flip: bold when unfair, timid when favorable

What makes one strategy optimal? Siegrist gives a single sufficient condition. A strategy with success function V beats every other strategy if, at every fortune x and every allowable bet y, mixing a bet does not help.

$$ p\,V(x + y) + q\,V(x - y) \le V(x) $$

In words: the chance-weighted average of where a bet of size y could land you, winning to x plus y or losing to x minus y, must be no greater than staying put in value terms. This is a concavity-flavored test, and which strategy passes it depends entirely on the sign of the edge. When the game is favorable, p at least one half, the timid success function satisfies the condition and timid play is optimal; with a real edge you want maximum exposure to your advantage, so you bet as small and as often as the house allows and let the edge compound. When the game is unfair, p at most one half, the bold success function satisfies it instead and bold play is optimal; with a disadvantage you want minimum exposure, so you resolve the bet in as few games as possible.

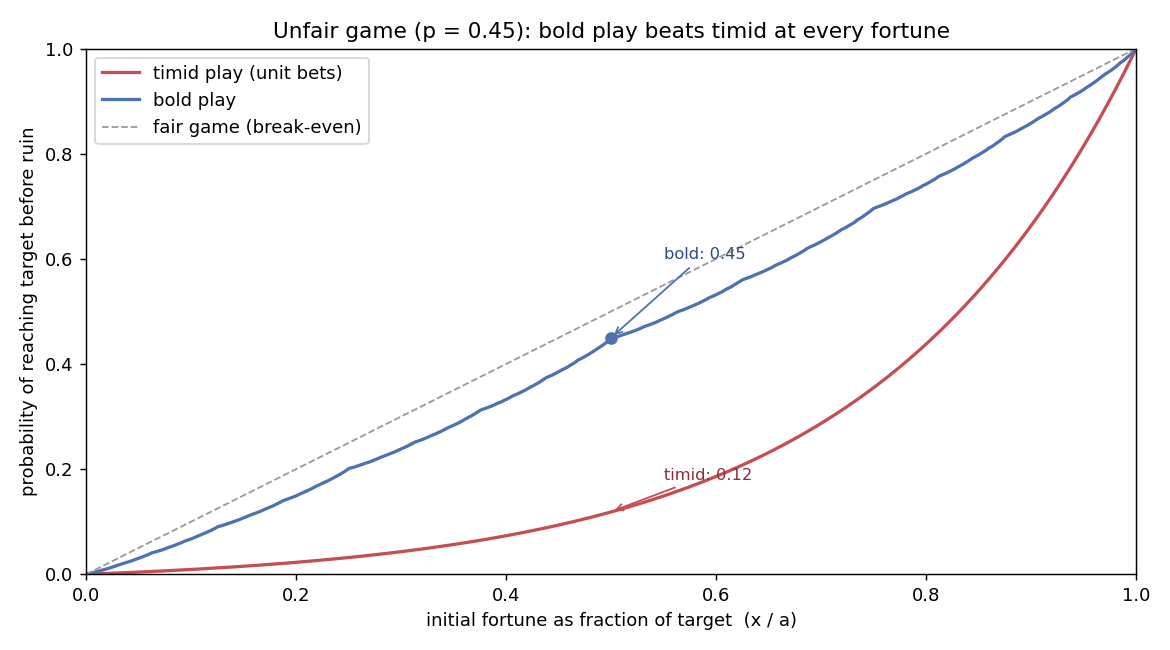

The generated figure puts the two head to head in the unfair case at p equal to 0.45. Bold sits above timid at every single starting fortune, and the gap is brutal near the middle: from half your target, bold reaches the goal 45 percent of the time while timid manages 12 percent. There is a final twist Siegrist proves and I will only flag: in the unfair case bold is not the unique optimum. An entire infinite family of higher-order bold strategies, built by rescaling the basic one, achieves the identical success probability. So "bet boldly" is really "resolve the game fast," and there are many ways to do that equally well.

What this actually means for a trader

Strip away the elegance and the practical warning is sharp. Bold play maximizes the probability of hitting a fixed target before ruin. It does not maximize growth, it does not maximize expected wealth, and it cheerfully accepts near-certain ruin in exchange for a better shot at the goal. That is the opposite objective from Kelly. Kelly, the subject of the old article "Kelly Rejects Bad Trades Automatically: Why Overbetting Kills and Underbetting Doesn't," maximizes long-run growth on a favorable edge and structurally refuses to risk total ruin. Bold play is what you reach for precisely when Kelly has nothing to offer, because your edge is zero or negative and there is no long run to grow into, only a target and a barrier.

A funded-account challenge is this problem wearing a suit. You must reach a profit target before hitting a drawdown floor, and after fees, spread, and slippage your per-trade edge is often at or below break-even. The red-and-black theorem says your best chance in that spot is to concentrate risk, take a small number of large, decisive swings, not to grind a hundred tiny scalps that feed volume into a losing expectation. But read the theorem honestly. It tells you how to make the least-bad of a losing situation, not how to win. If your true edge is negative, bold play raises your pass probability from dismal to merely bad, and no bet-sizing rule invented can turn a house edge into money. The only durable fix is an actual edge, at which point the math flips and you should be betting timid anyway.

Where this connects

This is the geometry underneath the Kelly pillar. The old article "Kelly Rejects Bad Trades Automatically: Why Overbetting Kills and Underbetting Doesn't" showed Kelly sizing on a favorable edge to maximize growth; red-and-black is the mirror world where the edge is against you and the objective is a target, not growth, so the answer inverts to bold. The old article "Kelly in Prediction Markets vs a Prop Challenge: Same Formula, Opposite Geometry" already carried the gambler's-ruin barrier into a funded-account setting; this article supplies the theorem that says what to do once you are trapped behind that barrier.

The honest through-line is a warning about objectives. Before you copy a bet-sizing rule, check which quantity it maximizes. Kelly maximizes growth and protects against ruin. Bold play maximizes the probability of touching a target and embraces ruin as the price. Pick the wrong one for your situation and you will grind yourself out with tiny disciplined bets in a game where the only rational move was to swing once and get it over with, or you will blow up swinging in a game where patience would have compounded a real edge.

KEY POINTS

- In an unfair game, bold play, betting your whole fortune toward the target on each game, maximizes the probability of reaching a target before ruin. Timid grinding is provably the worst choice.

- The strategy flips with the sign of your edge: bold when the game is against you, timid when it favors you. It is proven by a single optimality condition, p times V of x-plus-y plus q times V of x-minus-y at most V of x.

- Every bet moves expected fortune by two-p-minus-one times the stake, so with a negative edge your total expected loss scales with total volume wagered. Minimizing exposure, not maximizing it, is the goal.

- Timid play is gambler's ruin: the success function is convex and floor-hugging when unfair. Starting at half a 20-dollar target with p equal to 0.45, you reach the goal only 12 percent of the time.

- Bold play scales and obeys a doubling-map functional equation. Its success function is a singular continuous staircase, continuous and strictly increasing yet with zero derivative almost everywhere, and it still sits below break-even in an unfair game.

- From half your target at p equal to 0.45, bold reaches the goal 45 percent of the time versus timid's 12 percent, and bold dominates timid at every starting fortune.

- Bold play maximizes hitting a target, not growth, and accepts near-certain ruin. It is the opposite objective from Kelly and is only the right tool when your edge is gone. It makes a losing game less lost, never won.

References

- Generalizations of Bold Play in Red and Black (Pendergrass and Siegrist, 2001)

- A New Interpretation of Information Rate (Kelly, 1956)

- How to Gamble If You Must (Siegrist, 2008, MAA Convergence)

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.